A Complete Guide to Choosing the Right Payment Method for Your Financial Life

In today’s cashless world, most people rely on credit cards and debit cards for everyday transactions. From buying groceries and paying bills to booking flights and shopping online, these two payment methods dominate modern personal finance. Yet despite their widespread use, many people still ask the same question:

Credit vs. debit: which is better?

The answer isn’t as simple as choosing one over the other. Credit and debit cards serve different purposes, come with different risks and benefits, and impact your financial life in very different ways. Understanding these differences is essential if you want to manage money wisely, avoid unnecessary debt, and build long-term financial stability.

This article provides a deep, practical, and balanced comparison of credit versus debit cards—covering how they work, their pros and cons, security issues, spending behavior, fees, credit scores, and real-world use cases—so you can confidently decide which option is better for you.

Understanding the Basics

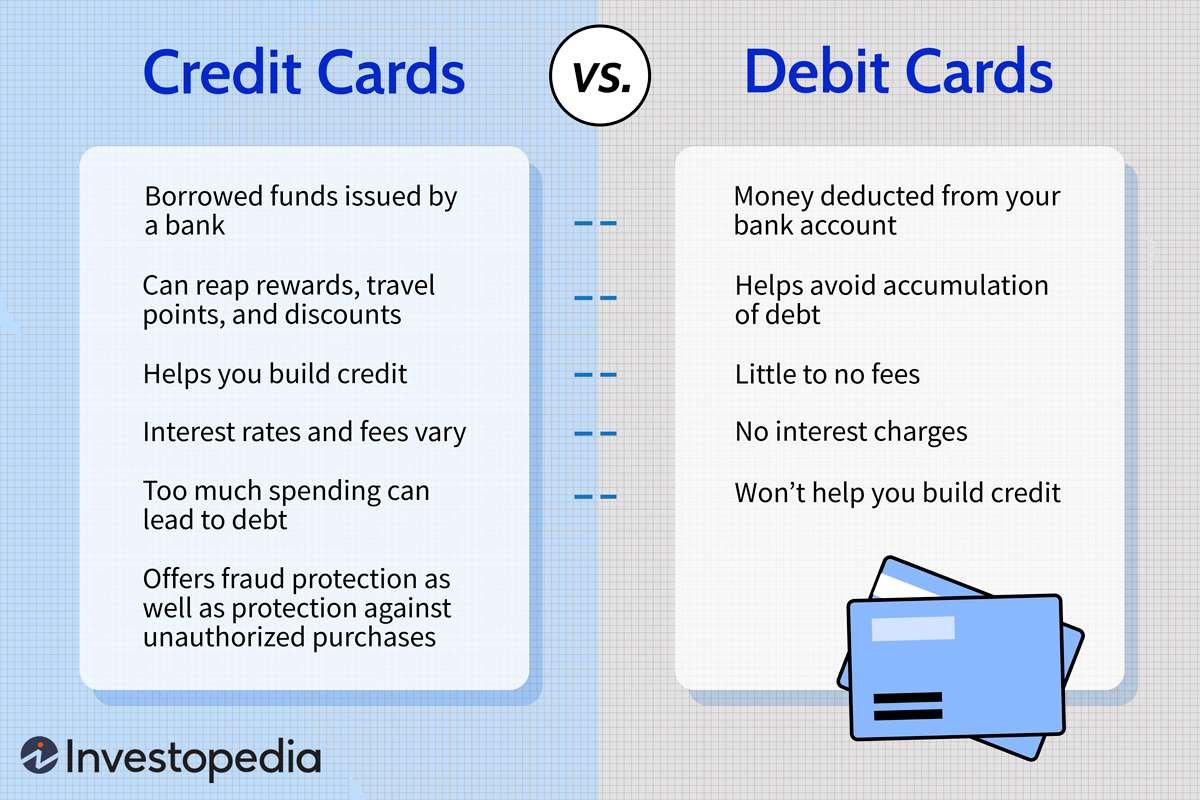

What Is a Debit Card?

A debit card is directly linked to your bank account. When you make a purchase using a debit card, the money is immediately withdrawn from your available balance.

Key characteristics:

- Uses your own money

- No borrowing involved

- Transactions are usually instant

- Spending is limited by your account balance

Debit cards are essentially a digital replacement for cash and checks.

What Is a Credit Card?

A credit card allows you to borrow money from a financial institution up to a certain limit. You repay the borrowed amount later, either in full or over time.

Key characteristics:

- Uses borrowed money

- Comes with a credit limit

- Requires monthly payments

- May charge interest if not paid in full

Credit cards are short-term loans disguised as payment tools.

How Credit and Debit Cards Work in Daily Life

Debit Card Transactions

- Funds are deducted immediately or within a day

- Account balance decreases instantly

- Overspending is limited unless overdraft is enabled

Credit Card Transactions

- Charges accumulate throughout the billing cycle

- Payment is due at the end of the cycle

- Interest applies if balance is carried forward

This fundamental difference—spending your money vs. borrowing money—drives almost every other comparison between credit and debit.

Spending Control: Credit vs. Debit

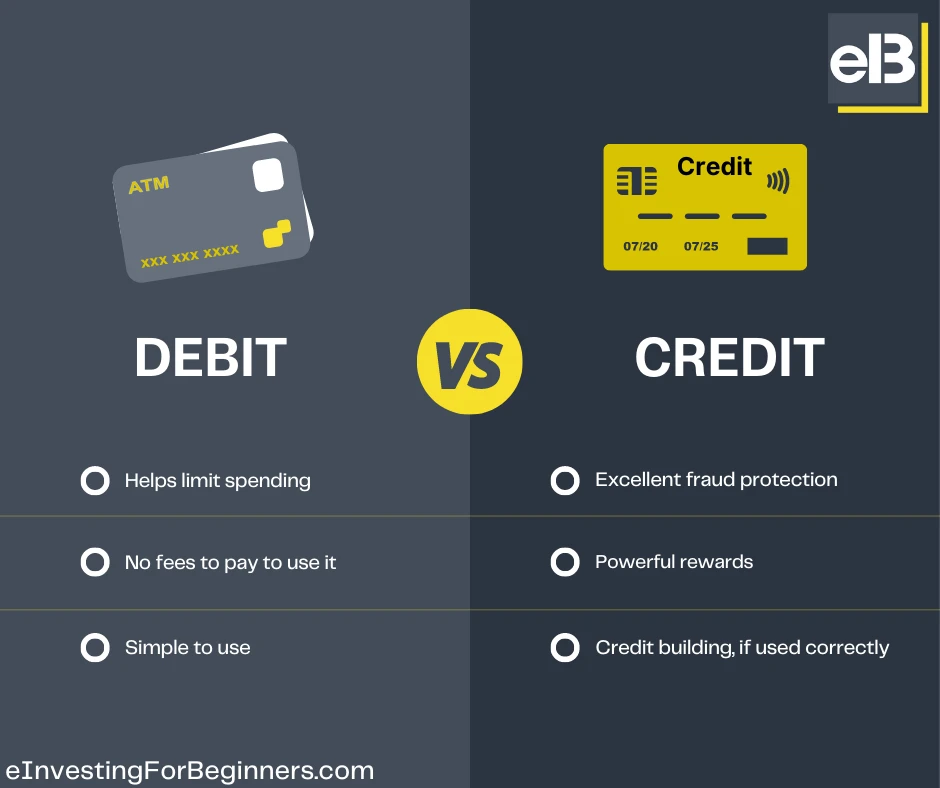

Debit Cards and Spending Discipline

Debit cards naturally limit spending because:

- You can only spend what you have

- There is no temptation to “borrow now, pay later”

This makes debit cards ideal for:

- Budget-conscious users

- Students and beginners

- People recovering from debt issues

Credit Cards and Spending Flexibility

Credit cards provide flexibility:

- Useful for emergencies

- Helpful when cash flow is uneven

However, flexibility can become a trap:

- Overspending is easier

- Monthly bills can pile up quickly

Studies consistently show that people tend to spend more using credit cards than debit or cash.

Impact on Your Credit Score

Debit Cards: No Credit Impact

Debit card usage:

- Does not affect your credit score

- Is not reported to credit bureaus

Using a debit card responsibly does nothing to build your credit history.

Credit Cards: Credit-Building Power

Credit cards directly impact your credit score through:

- Payment history

- Credit utilization

- Length of credit history

Responsible credit card use can:

- Improve your credit score

- Help qualify for loans and mortgages

- Lower interest rates in the future

This is one of the strongest arguments in favor of credit cards.

Fees and Costs Comparison

Debit Card Fees

Possible fees include:

- ATM withdrawal fees

- Overdraft fees

- Foreign transaction fees

Most debit cards have low or no monthly fees, especially with basic bank accounts.

Credit Card Fees

Credit cards may include:

- Annual fees

- Interest charges

- Late payment fees

- Cash advance fees

Interest rates on credit cards are often very high, especially if balances are not paid in full.

Security and Fraud Protection

Debit Card Security

Debit cards offer fraud protection, but:

- Fraudulent transactions may drain your bank account

- Recovering funds can take time

This can cause short-term cash flow problems.

Credit Card Security

Credit cards generally offer:

- Strong fraud protection

- Easier dispute processes

- No immediate impact on your bank balance

For online shopping and travel, credit cards are often safer.

Rewards and Benefits

Debit Card Rewards

Some debit cards offer:

- Cashback

- Merchant discounts

However, rewards are usually minimal.

Credit Card Rewards

Credit cards often provide:

- Cashback

- Travel points

- Airline miles

- Purchase protections

If managed correctly, rewards can provide real value.

Psychological Effects of Credit vs. Debit

Debit Encourages Mindfulness

Because money leaves immediately, debit users:

- Feel the cost more strongly

- Tend to spend less

Credit Encourages Detachment

Delayed payment reduces the psychological “pain of paying,” often leading to higher spending.

Using Credit vs. Debit for Different Situations

Everyday Expenses

Debit is better for:

- Groceries

- Utilities

- Daily transport

Large Purchases

Credit may be better for:

- Electronics

- Furniture

- Emergency expenses

Especially when payment plans or protections are needed.

Online Shopping

Credit cards offer stronger fraud protection.

Travel

Credit cards are usually preferred due to:

- Hotel and rental car requirements

- Travel insurance

- Better exchange rates

Debt Risk: The Biggest Difference

Debit Cards: No Debt

With debit:

- You cannot accumulate debt

- Overspending is limited

Credit Cards: High Debt Potential

Credit cards can:

- Create long-term debt

- Accumulate high interest

- Damage credit scores if misused

Discipline is essential.

Who Should Use Debit Cards More Often?

Debit cards are better for:

- Students

- People on strict budgets

- Those avoiding debt

- Individuals with poor spending habits

Who Benefits Most from Credit Cards?

Credit cards are better for:

- People with strong financial discipline

- Frequent travelers

- Individuals building credit

- Those who pay balances in full monthly

Credit vs. Debit: A Side-by-Side Comparison

| Feature | Debit Card | Credit Card |

|---|---|---|

| Uses your money | Yes | No |

| Builds credit | No | Yes |

| Risk of debt | None | High |

| Rewards | Limited | Strong |

| Fraud protection | Moderate | Strong |

Common Myths About Credit and Debit Cards

Myth 1: Credit Cards Are Always Bad

Reality: They are powerful tools when used responsibly.

Myth 2: Debit Cards Are Always Safer

Reality: Debit fraud can be more disruptive short-term.

Myth 3: You Must Choose One

Reality: The best strategy is often using both.

Smart Strategy: Using Credit and Debit Together

A balanced approach:

- Use debit for daily spending

- Use credit for planned purchases and rewards

- Pay credit balances in full every month

- Track all spending regularly

This strategy combines control and benefits.

Common Mistakes to Avoid

- Carrying a credit card balance

- Ignoring fees

- Using credit for impulse purchases

- Relying only on one payment method

Final Verdict: Which Is Better?

So, credit vs. debit—which is better?

The real answer is: neither is universally better.

- Debit cards are better for control, simplicity, and avoiding debt.

- Credit cards are better for flexibility, protection, rewards, and credit building.

The best choice depends on your financial habits, discipline, and goals.

When used wisely, credit and debit cards are not enemies—they are complementary tools that can help you manage money smarter and live more financially confident.

Summary:

Most people either personally own or at least know about credit cards. Credit cards are small, rectangular pieces of plastic that can be used to purchase items in stores and on the Internet in place of cash. All of the many different types of credit cards in existence come with very specific and individual credit terms and conditions that state when payments must be made on credit balances, how much interest must be paid on out-standing credit balances, and what will happen t…

Keywords:

credit, credit card, debit, debit card, interest, IPR, charges, bank statements

Article Body:

Most people either personally own or at least know about credit cards. Credit cards are small, rectangular pieces of plastic that can be used to purchase items in stores and on the Internet in place of cash. All of the many different types of credit cards in existence come with very specific and individual credit terms and conditions that state when payments must be made on credit balances, how much interest must be paid on out-standing credit balances, and what will happen to a credit card holder if payments are not made on time � which usually consists of the need to pay late fees.

Credit cards have, over the course of several decades, become the preferred method of payment for individuals across the Untied States and even the entire world because they are easy to use, convenient, relatively simple to obtain, and they can allow for purchases that would otherwise be unaffordable. In most cases, credit cards are beneficial and a true asset to the economy.

However, when credit cards are abused by being used too often and to purchase items that are extremely expensive, consumers can get themselves into a heap of financial trouble. The most common problems that people have with credit cards are that they charge much more than they can afford, and become severely in debt. It can take some people years to recover from high credit card balances.

A good alternative for individuals who either have bad credit or who do not want to own the responsibility that comes along with a credit card are prepaid charge cards or debit cards. The basic concept behind a prepaid charge card is that it does not allow a person to spend money they do not have, while still providing the convenience of the small, rectangular piece of plastic that is so much more convenient than cash.

A pre-paid charge card is associated with an account that has money in it. Each time the pre-paid charge card is used, money is electronically withdrawn from that account. The account holder can add money to their pre-paid charge account at any time, or money can be automatically transferred from another a separate account on a scheduled basis. Normally, the charge card agency charges the account holder a small fee each time the card is used or they may charge a small monthly fee. Sometimes, there are no fees associated with the card at all.

Prime candidates for pre-paid charge cards are people who have owned a credit card and have developed bad credit, young adults who have never owned a credit card and need practice, parents who want to give a card to their children but do not trust them with official credit, and people who never seem to have cash on hand.

One of the best aspects of most pre-paid charge cards is that they look very similar (if not identical) to regular credit cards. Therefore, if a person has a pre-paid charge card due to the fact that he or she has bad credit, people who see the card will probably not know the difference.

Debit cards are very similar to pre-paid charge cards except that they are normally associated with a persons regular checking or savings account at their local bank. While a debit card may have a Visa or MasterCard logo on it, when the credit card is used, money is automatically withdrawn from the person�s checking or savings account.

Debit cards may or may not have fees associated with them, and the terms and conditions associated with debit cards will vary depending on a person�s bank. Often, banks offer good deals on debit cards if a person agrees to have his or her regular payroll check directly deposited into their checking or savings account on a bi-weekly or monthly basis.

Before deciding on a regular credit card, a pre-paid charge card or a debit card, check out all of the available options available via the Internet and local banks. There are hundreds of options, and there is sure to be an alternative that fits best with any individual�s needs.

Tinggalkan Balasan